MALAYSIA: Obstacles May Reduce Future Palm Oil Production Growth

For the past 30 years Malaysia has been a world leader regarding organizing an efficient and highly productive commercial oil palm plantation sector, as well as in pioneering important agricultural research and varietal development that benefited palm oil producers throughout the region. As a result of the coordinated efforts of government and commercial companies over this extended period (1979-2010), Malaysian palm oil production increased roughly 600 percent – averaging 7 percent growth per annum. Malaysia was the world’s leading producer and supplier of palm oil and its various by-products for much of this period, only recently being eclipsed by its neighbor Indonesia. The strength and continuity of the 3 decades-long growth cycle was a remarkable achievement, being a product of substantial financial investment, a large pool of skilled immigrant labor, and extensive land areas suitable for conversion to plantations.

However, in the last couple of years it has become apparent that the era of rapid growth may be coming to an end as a variety of physical obstacles and government policies have begun to weigh on the palm oil industry’s productivity. As a result, the prospect of stagnating future output from the world’s second largest palm oil producer may be virtually unavoidable. This outcome would be a real concern to the international edible oil market, given there are few if any other nations in the short-term which are capable of adequately boosting supply.

Annual global palm oil demand has increased at roughly 2.3 million tons per year over the past 10 years, with Malaysia supplying nearly 30 percent of the increase in production required to meet this demand. Indonesia has supplied 62 percent. Other countries supplied the remaining 8 percent. With intense pressure being brought to bear on the Indonesian government to halt or slow its own oil palm plantation expansion owing to international environmental and greenhouse gas concerns, the prospect of stagnating Malaysian production substantially increases the likelihood of sustained high prices in the edible oil market. Since palm oil is the world’s cheapest edible oil, it has become the primary cooking oil for the majority of people in the developing world of Asia, Africa, and the Middle East. The consumer base in these regions is large, growing, poor, and highly price-sensitive. Given there are currently no viable and affordable alternatives to palm oil for most of these consumers, any significant reduction in the growth rate of Malaysian production will make it difficult for them to increase the use of edible oils in their diets.

Declining Availability of New Lands

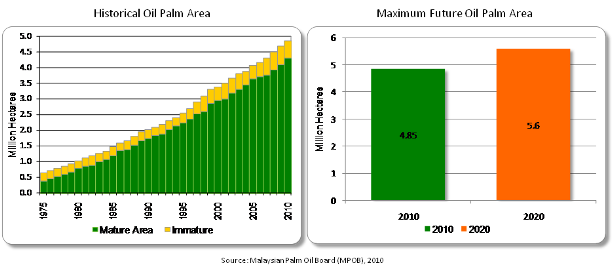

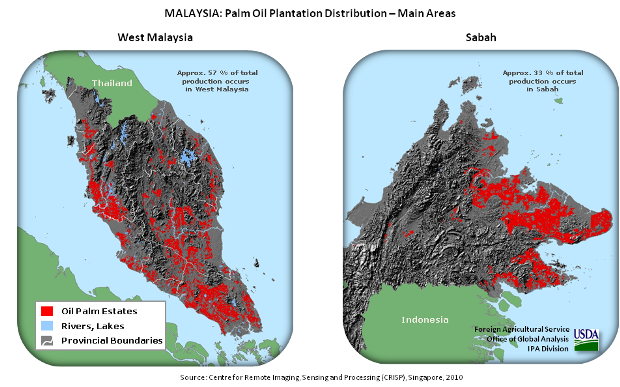

Malaysian palm oil companies have engineered a sustained long-term expansion of plantation area, increasing 3.85 million hectares since 1980 or 385 percent. Much of this development has been at the expense of native tropical forest, with national forest cover in core palm oil producing areas declining dramatically over the same period. In 2010 the government estimated that approximately 58 percent of the total national land area remained forested, and that its official policy is to keep 50 percent of the country forested in perpetuity. Therefore, time and land availability is quickly running out for the palm oil industry. The reality is that virtually all highly suitable areas have already been developed, and that even marginal land is now becoming scarce. The province which reportedly has the most remaining development potential is Sarawak, though much of the available land is low-lying coastal peatland and/or degraded inland forest with native claims.

The Malaysian industry indicates that owing to these constraints national palm oil area will likely peak at roughly 5.6 million hectares by 2020, meaning there is only about 750,000 hectares left for future expansion. At current annual growth rates of 180,000 hectares per year, that leaves Malaysian planters with about 6 years before they run out of land. In fact, Malaysian companies have long since recognized that time is growing short for expansion domestically, and as a result have radically increased oil palm investments and landholdings in other countries such as Indonesia and Liberia. Malaysian companies have collectively established over 1.0 million hectares of active oil palm plantations in Indonesia and own a further 1.0 million hectares of land (land bank) which has official permits allowing its development in the future. As a result of these sizable investments, Malaysian conglomerates have become the 2nd largest commercial palm oil enterprises in Indonesia – behind only the Indonesian companies themselves.

Stagnating National Yields

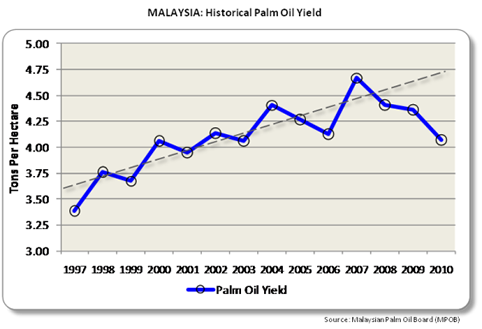

Another issue which indicates that future palm oil production growth may slow is the recent stagnation of national yields, despite the availability of ample financing, crop inputs, and agronomic knowledge. Trend yield growth prior to 2008 had been strong, averaging roughly 4 percent per year. But since then average national yields have unexpectedly declined by about 13 percent.

A number of factors have reportedly led to the sharp fall off in average yields over the past 4 years, including adverse weather (El Nino - drought, La Nina – heavy rains), declining fertilizer use, and low replanting rates. It is estimated that 25-30 percent of Malaysian oil palm trees are 20-30 years old (past the peak period of yields), and that high international prices have suppressed normal replanting rates. Growers are reportedly loathe to replace actively producing trees at a time of record profits with young seedlings which require nearly 7 years to equal their output. Taking area out of production for 3 or more years just doesn’t make good economic sense under the circumstances. The genetic yield potential of the older trees is also significantly lower than that of cultivars available today and to new clonal varieties being developed. The longer the lag in replanting these older cultivars, the greater long-term delay in improving national average yields.

In addition to these factors, reports have surfaced that skilled labor shortages have plagued some regions, reducing harvest activity by 50 percent and leaving ripe but un-harvested fruit rotting on the plantation. The growing labor problem may be the largest issue facing the industry, as palm oil estates rely heavily on immigrant Indonesian workers. The Malaysian Employer’s Federation reports that at least 80 percent of oil palm estate employees are of Indonesian nationality. At the same time, robust growth in plantings in Indonesia are creating lots of jobs for skilled plantation workers and causing acute competition for labor. Wage pressure is reportedly hitting Malaysian plantations as they compete for needed manpower. Given future growth prospects in the palm oil industry in Indonesia, this problem will continue for Malaysian producers unless wages and benefits rise significantly and restrictive Malaysian immigration laws are amended.

In any case a return to historical trend yield growth is not expected soon, unless and until a major replanting campaign has been completed. The government reports that current annual replanting rates average 3-4 percent of the total national area, and that it will take approximately 25 years to replant the entire national acreage.

Production Growth Uncertain

Over the next 6-10 years while Malaysia’s oil palm acreage continues to expand, it is still expected to marginally increase annual palm oil production. Over that period, assuming average yields range between 4.0-4.2 tons per hectare, total annual production may increase a total of 5-6 million tons over current levels. But thereafter production should stagnate until there has been considerable progress in replacing older trees with new higher yielding (HYV) clonal and non-clonal varieties. Industry officials indicate that currently available HYV cultivars can yield 50-75 percent higher than those they would be replacing, so there is real potential to achieve substantial future growth in national production once 25-50 percent of the national crop has been replanted. Assuming Malaysia can resolve its labor issues, it is simply a matter of time before the country can once again achieve strong and reliable productivity growth and sufficient palm oil production to help offset rising global demand. Before this happens however, Malaysia may underperform for a considerable number of years. Replanting rates are currently well-below industry-recommended levels and international palm oil prices and profits are both very high. As long as these conditions are sustained there is an increased likelihood that Malaysia will take considerably longer to achieve the growth rates it is inherently capable of.

Current USDA area and production estimates for grains and other agricultural commodities are available on IPAD's Agricultural Production page or at PSD Online.

|